The argument that runs through most long-term money struggles isn’t really about financial literacy. It’s about something that happened before most people could read.

A 2013 study by researchers at Cambridge University found that core money habits are typically formed by the age of seven. Those behaviors – including emotional responses to spending, saving, and planning – often persist into adulthood. Before allowances, before any formal lessons in personal finance, before most children have any idea what a mortgage is. The habits are already in place.

For people who grew up without much money, those early-formed habits carry a particular weight. The experience of tight budgets and insecure income requires a constant focus on immediate and pressing shortages, which limits the ability to plan, make decisions, or consider long-term goals. The brain adapts to that environment. And the adaptations that made sense in a childhood of scarcity don’t simply dissolve once the bank account stabilizes in adulthood. They go underground. They surface in ways that are often confusing, even to the person experiencing them – a flash of panic at the checkout, a strange guilt after a restaurant meal, a refrigerator stocked like a hurricane is coming.

The following 11 behaviors are not character flaws. They’re the fingerprints of a specific kind of upbringing, described by researchers who study poverty behaviors and the money mindset that forms in early life. Some of them you might recognize immediately. Others might take a moment – and then land harder for the delay.

1. Stockpiling Food and Household Goods

The pantry that’s overflowing long after the scarcity is over. The extra cans of soup pushed to the back of the shelf. The instinct to buy a second pack of something because you remember when there was none. Food hoarding behavior in adults who grew up in low-income households is well-documented, and it originates in something entirely rational: when food ran out as a child, the consequences were real.

According to Harvard Magazine’s profile of behavioral economist Sendhil Mullainathan’s scarcity research, poverty redirects attention toward urgent demands while reducing the mental capacity available for everything else – effectively reshaping how all decisions get made. Scarcity, Mullainathan and co-researcher Eldar Shafir found, loads the mind with so many background concerns that it leaves less cognitive capacity for the task in front of you, much like too many programs running at once slow a computer to a crawl. The refrigerator packed tighter than it needs to be isn’t irrational. It’s the body and brain maintaining a buffer against a threat that no longer exists. Knowing that intellectually doesn’t make the urge disappear. For many people, a well-stocked kitchen remains one of the few reliable signals that things are okay.

The same pattern extends beyond food. Toiletries bought in bulk, a closet full of practical items purchased at a discount “just in case,” an extra blanket stored somewhere no one uses – all of it is the same impulse in different clothes. The logic of scarcity built that behavior, and it takes more than a steady income to dismantle it.

2. Guilt After Spending Money, Even on Necessities

Buying a new pair of shoes when the old ones still technically work. Ordering something at a restaurant and immediately calculating whether you should have. Feeling a knot in your stomach after a grocery run that ran slightly over budget. For people raised in financial hardship, the sensation after spending money isn’t neutral. It tends toward guilt, worry, or a vague sense that something just went wrong.

A 2024 NerdWallet study found that 28% of Americans are anxious about their finances even though they have enough to live comfortably and save for the future, and that for many, financial stress and money worries can be completely uncorrelated with the amount of money they actually have. The spending guilt that formed when money was genuinely short doesn’t automatically recalibrate when the situation improves. The trigger is already wired in. A purchase that a financially comfortable friend makes without a second thought can feel almost transgressive to someone who grew up calculating whether the family could afford bread at the end of the month.

The guilt is often invisible to others, which means it gets carried alone. The internal monologue running through every checkout interaction rarely makes it into conversation.

3. Difficulty Throwing Things Away

The broken appliance sitting in the garage for three years because it might be fixable. The clothes that don’t fit anymore, kept because they weren’t cheap and might fit again someday. The drawer full of rubber bands, twist ties, and takeout napkins. Growing up in a household where nothing was wasted leaves a very specific imprint, and it doesn’t always ease once the material circumstances change.

Experiencing financial hardship during childhood can leave adults in a state of constant low-level vigilance, always braced for a return to insecurity. That vigilance drives collecting and keeping – hoarding objects against an imagined future shortage, avoiding financial risk, staying cautious with spending long past the point where caution is necessary. The object being kept isn’t the point. The object is standing in for security. Throwing it away means accepting that if you need it again, you’ll be able to replace it – and for someone whose childhood didn’t confirm that safety net, that trust is hard to extend.

This is one of those poverty behaviors that the money mindset literature consistently identifies as sticky. It often feels virtuous from the inside (“I’m just not wasteful”) and excessive from the outside, which makes it particularly resistant to examination.

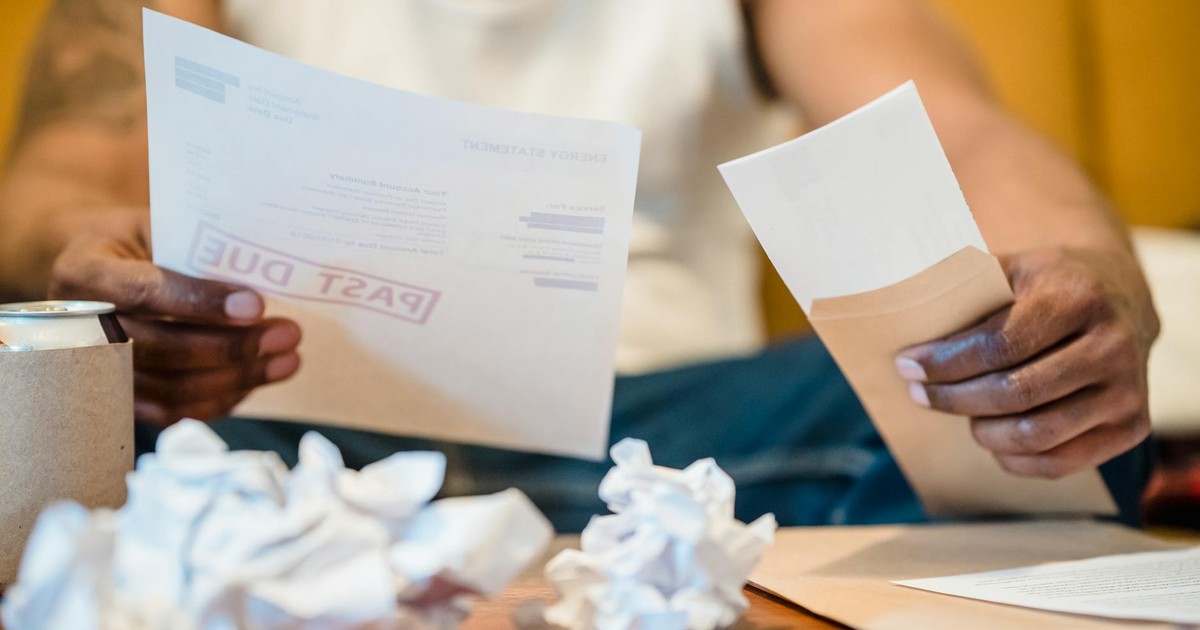

4. Treating Every Unexpected Bill as a Crisis

A car repair estimate. A medical copay that’s higher than expected. A heating bill that came in over the usual amount. For most adults with financial stability, these are inconveniences. For people raised without much money, they can trigger a disproportionate alarm response – a racing heart, a sleepless night, a spiral of catastrophizing about what comes next.

The UAB Institute for Human Rights describes this as a learned prioritization pattern: when people operate under conditions of constant scarcity, the mind trains itself to treat all financial surprises as emergencies, because once they genuinely were. That pattern of narrowing hard under financial threat was practiced repeatedly in childhood. It becomes a default response even when the circumstances no longer warrant it. The nervous system learned to escalate quickly because, once, quick escalation was the difference between managing the problem and not managing it at all.

Adults who grew up in households where an unexpected expense genuinely could derail the family often describe feeling like a fraud after they’ve become more financially stable – stable enough on paper, but still waiting for the other shoe to drop.

5. Reflexively Saying “I Can’t Afford That”

Before checking the price. Before looking at the account balance. Before doing the math. The phrase comes out automatically, a social habit more than a financial statement. People who spent years hearing that phrase, or saying it themselves to avoid wanting things they couldn’t have, often carry it into adulthood as a kind of verbal reflex – one that sometimes stops them from accessing things they could actually afford.

Research published in 2024 found that childhood socioeconomic position relates to greater temporal discounting and steeper devaluation of future rewards in adulthood – meaning people who grew up with less are statistically more likely, as adults, to undervalue future gain and overweight immediate cost. These findings held across a cohort of nearly 13,000 adults from 61 countries, and remained significant even after accounting for education level and current employment. “I can’t afford that” is sometimes a genuine financial statement. More often, for this group, it’s a posture – a pre-emptive closing of the door before disappointment can walk through it.

The behavior is self-protective. It also, when it becomes automatic, can prevent people from investing in things that would actually improve their circumstances, from professional development to basic home maintenance.

6. Spending in Bursts After a Period of Restraint

The flip side of chronic scarcity isn’t always more scarcity. For some people raised without much money, the experience of finally having a bit more produces a spending pattern that looks almost opposite to their usual caution: a burst of spending, often on things that feel symbolic rather than practical, followed quickly by guilt and a snap back to restriction.

When people live paycheck to paycheck, their attention gets pulled entirely toward urgent concerns, and long-term planning becomes almost impossible to hold onto. When the pressure briefly lifts, the system doesn’t immediately know what to do with the slack. Spending on something – anything – can feel like proof that things have changed, even when that spending undermines the financial progress that created the breathing room in the first place. It’s a cycle that financial therapists recognize immediately but that can look, from the outside, like simple impulsiveness.

7. Struggling to Ask for or Accept Help

The reluctance to ask for a loan even in a genuine emergency. The discomfort when someone offers to pick up the tab. The insistence on handling everything alone even when help is both available and offered freely. For many who were taught to constantly worry about money, or who lived in an atmosphere where struggle was always present, accepting gifts or financial contributions from others becomes complex and confusing well into adulthood.

There’s shame woven into this one, and that shame has a specific texture. It’s not just about pride. It’s about the fear that accepting help confirms something that the person has worked very hard to leave behind – that they are someone who needs help, that they are, in some fundamental way, still in that childhood situation. Keeping the help at arm’s length is a way of maintaining the story that things are fine. That story can be very expensive.

The research is clear on one point: how upbringing shapes adult behavior doesn’t stop at money. The difficulty accepting support of any kind – emotional, practical, financial – is a pattern that often originates in households where asking for help was either pointless or actively discouraged.

8. Always Defaulting to the Cheapest Option

Not as careful comparison shopping, but as an automatic, non-negotiable rule. The store brand every single time. The cheapest flight, even when the layovers add six hours to the journey. The reluctance to pay more for something that would genuinely be better, longer-lasting, or more comfortable – because spending more feels wrong, feels like showing off, feels like gambling with money that should be kept in reserve.

When spending more was never an option in childhood, the decision itself can feel off-limits as an adult, even after circumstances have changed. What reads as frugality often runs deeper than a preference for saving. It’s a trained response to an environment where the premium option was simply not on the table, and where wanting it felt like a form of foolishness.

This behavior occasionally produces genuine savings. More often, it produces the paradox of buying the cheaper version of something three times instead of the more expensive version once.

9. Finding It Hard to Plan Financially Beyond the Short Term

Contributing to a retirement account feels abstract when you grew up focused on making it through the week. The 20-year investment horizon that personal finance advisors recommend doesn’t feel real to someone whose family was focused on the next 20 days. Long-term financial planning requires a kind of trust in the future – trust that things will be stable enough, that the plan will still be relevant, that there’s a point in deferring reward.

People who grew up in genuine financial instability often have good reasons not to trust that the future will resemble the present. Economic disruption wasn’t hypothetical in their childhood – it was the baseline. Planning for a retirement that is thirty years away requires believing, at some level, that thirty years of relative stability is a reasonable expectation. That belief is harder to build when early experience suggested otherwise.

10. Keeping Money Secrets, Even from Partners

The credit card that one person in a relationship doesn’t know about. The checking account balance not mentioned when someone asks. The vague, deflecting answer when a partner asks how things are going financially. Money talk, in many low-income households, was either charged with tension or absent entirely. According to the 2024 NerdWallet survey, just 30% of Americans say their family talked about money when they were growing up. For those who grew up in households where money meant stress, silence, or conflict, the habit of keeping financial information close becomes a self-protective reflex that follows them into their adult relationships.

This behavior can do real damage to financial partnerships and marriages. It’s also, when you trace it back, completely understandable. If money conversations in childhood reliably ended in argument, panic, or shame, the adult impulse to avoid them is straightforward: keep it separate, manage it alone, don’t let it contaminate the relationship. The problem is that this strategy usually produces exactly the outcomes it was designed to prevent.

11. An Unease Around Wealth or Expensive Environments

Walking into a high-end restaurant and feeling like a fraud. The immediate self-consciousness in a room where everyone else seems comfortable with their surroundings. The assumption, not always conscious, that wealthy spaces have unwritten rules that you don’t know and will eventually violate. People who grew up without much money often describe a specific discomfort in environments coded as expensive – not envy, exactly, but a low-level social anxiety about belonging there.

Social and economic deprivation during childhood and adolescence can have a lasting effect. Because the negative effects of deprivation on human development tend to accumulate, individuals with greater exposure to poverty during childhood are likely to face more difficulty navigating class-coded environments in adulthood. Class is a social identity as much as an economic one, and people who crossed economic lines as adults often report carrying both identities at once – able to afford the room, but still waiting to be found out. The discomfort isn’t irrational. It developed in real social environments where the signals of class were meaningful, where the wrong clothes or the wrong accent actually did close doors. That vigilance doesn’t disappear when the income bracket changes.

Researchers call this a kind of code-switching cost – the ongoing cognitive and emotional effort of operating in social contexts that don’t match your origins. It registers as exhaustion after events that should feel celebratory.

Read More: Little-Known Money Rules That the Wealthy Don’t Want You to Know

What to Do With All of This

None of these behaviors means anything is broken beyond repair. Most of them, looked at honestly, are fairly sensible responses to an environment that demanded them. The problem isn’t that these poverty behaviors and money mindset patterns exist. It’s that they often operate invisibly, driving decisions that feel instinctive but are actually borrowed from a set of circumstances that no longer apply.

The most useful thing, based on the research, isn’t to try to eliminate these patterns through sheer willpower. The money story is layered, shaped by experiences like parental arguments over bills, sudden financial shocks, or messages absorbed before you were old enough to question them. Reflecting on those influences isn’t about blame – it’s about recognizing patterns. Once you name what’s happening, you have a genuine choice about whether to act on it. The gap between noticing “I’m doing the thing again” and actually doing something different is where the real work happens. But you can’t close a gap you haven’t named.

Some of these patterns go back further than any individual financial decision. They go back to the first time you understood, as a child, that money was something to be afraid of. Naming that isn’t a solution. But it’s usually where an honest conversation with yourself about money actually starts.

AI Disclaimer: This article was created with the assistance of AI tools and reviewed by a human editor.